All Categories

Featured

Table of Contents

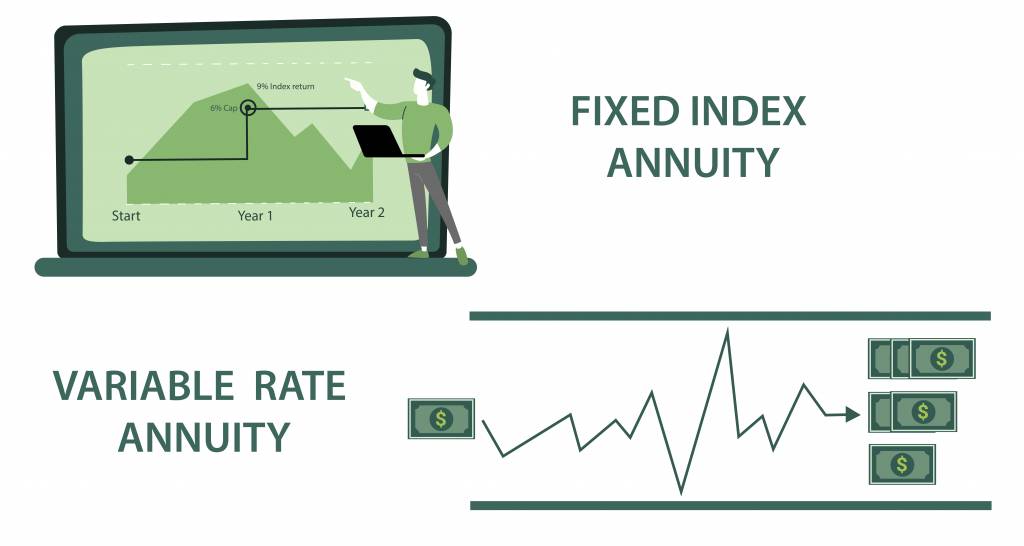

Your returns are based on the performance of this index, subject to a cap and a flooring.

This can provide an eye-catching equilibrium for those seeking moderate development without the higher danger account of a variable annuity. Immediate annuities: Unlike fixed annuities that start with a buildup stage, immediate annuities begin income repayments virtually immediately after the initial financial investment (or within a year at many). Called an instant income annuity, it is frequently selected by retired people who have already developed up their retired life cost savings are looking for a trustworthy means to produce regular earnings like a paycheck or pension plan settlement that starts right away.

If you believe a dealt with annuity may be the right alternative for you, here are some things to consider. Annuities can provide regular, foreseeable revenue for a set number of years or the rest of your life. Usually speaking, the longer you want repayments to last, the lower the amount of each repayment.

Survivor benefit: It is very important to consider what will occur to the cash in your taken care of annuity if you die while there's still an equilibrium in your account. A survivor benefit attribute enables you to assign a recipient who will obtain a defined quantity upon your fatality, either as a lump sum or in the form of ongoing settlements.

Certified annuities are moneyed with pre-tax bucks, typically through retirement like a 401(k) or IRA. Costs contributions aren't taken into consideration taxable revenue for the year they are paid, but when you take revenue in the distribution stage, the entire quantity is commonly based on taxes. Nonqualified annuities are moneyed with after-tax dollars, so tax obligations have currently been paid on the payments.

For instance, the Guardian Fixed Target Annuity SM offers a guaranteed price of return for three-to-ten year periods (all may not be offered at all times). You can choose the moment duration that best fits your retired life time framework. We can attach you with a local monetary professional that can describe your options for all kinds of annuities, assess the offered tax obligation advantages, and aid you decide what makes good sense for you.

Decoding How Investment Plans Work Key Insights on Your Financial Future Breaking Down the Basics of Variable Annuity Vs Fixed Indexed Annuity Features of Smart Investment Choices Why Choosing the Right Financial Strategy Is a Smart Choice What Is Variable Annuity Vs Fixed Annuity: Simplified Key Differences Between Immediate Fixed Annuity Vs Variable Annuity Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Vs Variable Annuities FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Retirement Income Fixed Vs Variable Annuity Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Fixed Income Annuity Vs Variable Growth Annuity A Closer Look at How to Build a Retirement Plan

Although several individuals very carefully determine the quantity of cash they'll need to live easily in retired life and invest their functioning years conserving for that objective, some still are afraid not having enough. As a matter of fact, due to raising life span, 60% of Americans are conc erned they might outlast their properties. This worry casts an even larger darkness on respondents already in or near retired life.

An annuity is an agreement in between you and an insurance provider that you can buy by paying a round figure or regular monthly costs. After the buildup period, the company gives a stream of payments for the remainder of your life or your selected period. Annuities can be a dynamic car to include in your retired life earnings mix, especially if you're concerned about lacking cash.

Decoding How Investment Plans Work A Closer Look at How Retirement Planning Works Breaking Down the Basics of What Is Variable Annuity Vs Fixed Annuity Advantages and Disadvantages of Fixed Vs Variable Annuity Pros Cons Why What Is Variable Annuity Vs Fixed Annuity Matters for Retirement Planning How to Compare Different Investment Plans: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing What Is Variable Annuity Vs Fixed Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Deferred Annuity Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Annuity Vs Equity-linked Variable Annuity

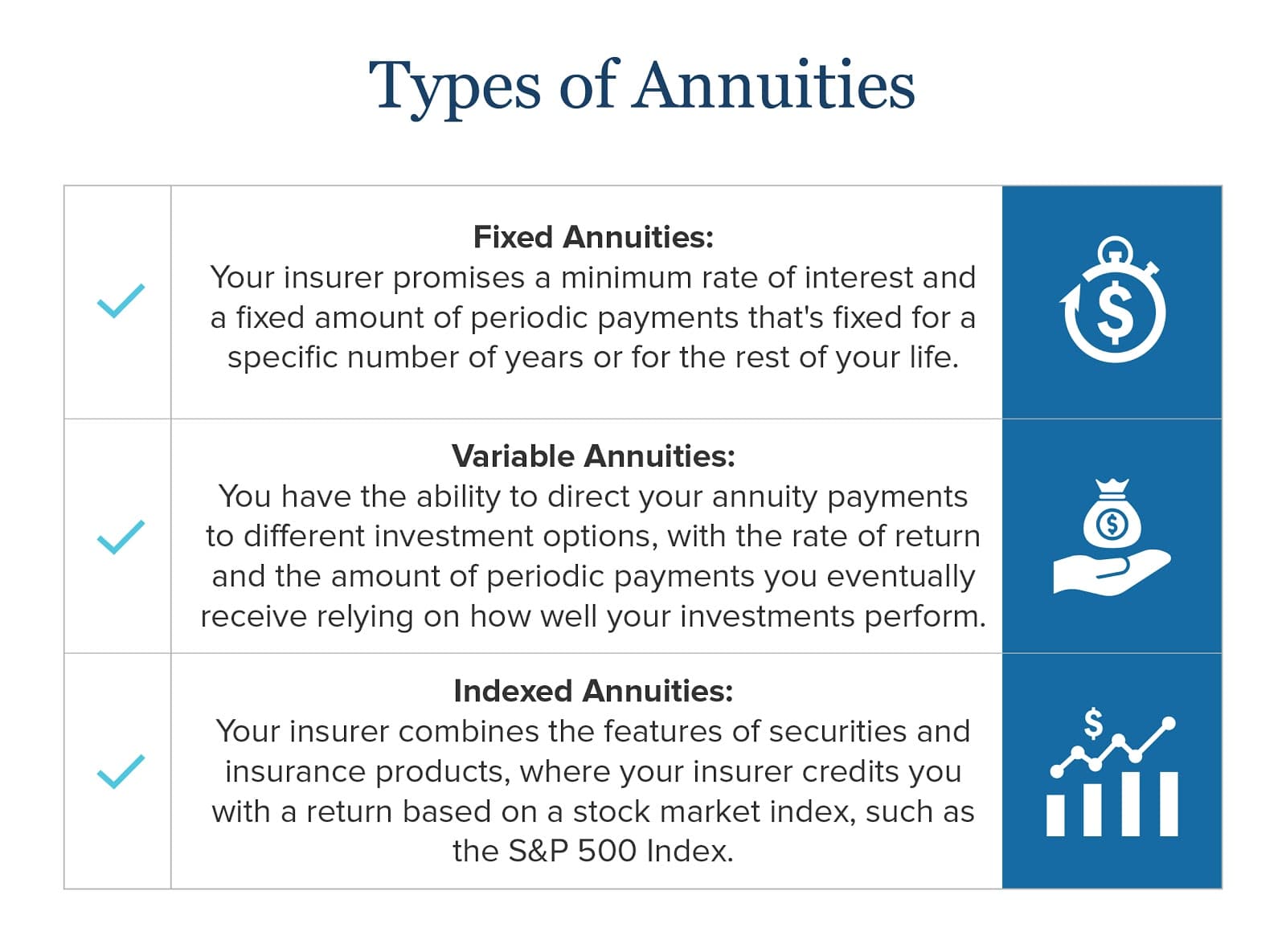

A fixed annuity is one of the most simple type, providing a dependable and predictable earnings stream. The insurance coverage firm guarantees a set rate of interest on your costs, which produces a steady income stream over the rest of your life or a certain duration. Like certificates of deposit, these annuities are often the go-to service for even more risk-averse investors and are among the best investment choices for retired life portfolios.

Your primary investment stays undamaged and can be passed on to enjoyed ones after fatality. Rising cost of living is a typical part of economic cycles. Typical dealt with annuities might lack protection from inflation. Fixed annuities have a stated rate of interest you gain no matter of the market's efficiency, which may indicate losing out on possible gains.

While you can take part in the market's benefit without risking your principal, taken care of index annuities limit your return. While you can acquire other annuities with a stream of payments or a swelling sum, instant annuities call for a lump sum.

Similar to the majority of annuities, you can determine whether to receive payments for a details period or the rest of your life. Immediate annuities supply a stable stream of revenue you can't outlive. These annuities are very easy to comprehend and take care of contrasted to various other financial investment products. You normally can't access your principal as soon as bought.

Right here are seven concerns to ask to aid you locate the right annuity. Take into consideration when you wish to start receiving annuity settlements. Immediate annuities have a brief or no accumulation duration, while deferred payment annuities can last over one decade. You have a number of options for the duration and kind of payments, consisting of fixed duration, lifetime, joint lifetime repayments, and swelling amount.

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Fixed Vs Variable Annuity Pros And Cons What Is Fixed Vs Variable Annuity? Benefits of Choosing the Right Financial Plan Why Choosing the Right Financial Strategy Is Worth Considering Deferred Annuity Vs Variable Annuity: Explained in Detail Key Differences Between Fixed Annuity Vs Equity-linked Variable Annuity Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Variable Vs Fixed Annuity Common Mistakes to Avoid When Choosing Fixed Indexed Annuity Vs Market-variable Annuity Financial Planning Simplified: Understanding Variable Annuity Vs Fixed Indexed Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at Immediate Fixed Annuity Vs Variable Annuity

You may desire to consider survivor benefit bikers to pass payments to your loved ones in the event of your fatality. Various annuities have various fees. Recognize the prices associated with your chosen annuity. Pick a reputable, reputable company with long-lasting security for included assurance. Contact economic ranking companies like Requirement & Poors, AM Best, Moody's, and Fitch.

Annuities can be intricate and confusing, also for skilled capitalists. That's why Bankers Life provides individualized advice and education throughout the process. We focus on understanding your needs and guiding you toward remedies to aid you achieve your ideal retired life. Interested in having a seasoned monetary professional review your circumstance and deal personalized insights? Contact a Bankers Life representative today.

Each individual must look for certain suggestions from their own tax obligation or legal consultants. To establish which financial investment(s) might be suitable for you, please consult your financial specialist prior to spending.

Both IRAs and postponed annuities are tax-advantaged methods to prepare for retirement. Annuities, on the various other hand, are insurance products that convert some financial savings right into ensured payments.

Review on for even more information and comparisons. An individual retirement account (INDIVIDUAL RETIREMENT ACCOUNT) is a kind of retirement financial savings lorry that permits financial investments you make to grow in a tax-advantaged way. They are a great method to save long-term for retired life. An individual retirement account isn't an investment in and of itself.

Decoding Fixed Vs Variable Annuity Pros And Cons Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Indexed Annuity Vs Fixed Annuity Why Choosing the Right Financial Strategy Is Worth Considering Pros And Cons Of Fixed Annuity And Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Key Features of Long-Term Investments Who Should Consider Fixed Income Annuity Vs Variable Growth Annuity? Tips for Choosing the Best Investment Strategy FAQs About Fixed Indexed Annuity Vs Market-variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Vs Variable Annuity

Often, these investments are stocks, bonds, common funds, or even annuities. Each year, you can spend a particular amount within your IRA account ($6,500 in 2023 and subject to transform in the future), and that financial investment will certainly expand tax cost-free.

When you withdraw funds in retirement, though, it's taxed as normal income. With a Roth IRA, the money you place in has already been exhausted, but it grows free of tax throughout the years. Those incomes can then be withdrawn free of tax if you are 59 or older and it has actually been at least five years since you initially contributed to the Roth individual retirement account.

Breaking Down Fixed Annuity Vs Variable Annuity Everything You Need to Know About Fixed Vs Variable Annuity Pros And Cons Breaking Down the Basics of Investment Plans Benefits of Variable Annuities Vs Fixed Annuities Why Choosing the Right Financial Strategy Is a Smart Choice Fixed Vs Variable Annuity Pros Cons: Explained in Detail Key Differences Between Tax Benefits Of Fixed Vs Variable Annuities Understanding the Key Features of Annuities Fixed Vs Variable Who Should Consider Fixed Interest Annuity Vs Variable Investment Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Fixed Vs Variable Annuity Pros Cons A Beginner’s Guide to Fixed Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

No. Individual retirement accounts are retirement financial savings accounts. Annuities are insurance coverage items. They work in completely different ways. You can occasionally place annuities in an IRA though, or utilize tax-qualified IRA funds to purchase an annuity. So there might be some crossover, yet it's the type of crossover that makes the essential differences clear.

Annuities have actually been around for a very long time, but they have actually ended up being more common recently as people are living longer, less individuals are covered by typical pension strategies, and preparing for retirement has ended up being more crucial. They can frequently be incorporated with other insurance policy products like life insurance policy to produce total protection for you and your family members.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Your Investment Choices A Closer Look at Annuities Variable Vs Fixed Defining Choosing Between Fixed Annuity And Variable Annuity Features of Smart Investment Choices Why Fixed Vs Variab

Decoding Fixed Vs Variable Annuity Everything You Need to Know About Variable Annuity Vs Fixed Annuity Defining the Right Financial Strategy Advantages and Disadvantages of Fixed Annuity Or Variable A

Decoding How Investment Plans Work Key Insights on Your Financial Future What Is Annuities Fixed Vs Variable? Advantages and Disadvantages of Different Retirement Plans Why Choosing the Right Financia

More

Latest Posts